By Jeff Bernier

It’s April in Atlanta—a season of yellow (pollen) cars, baseball spring training, the Masters golf tournament and, usually, taxes. As I am sure you know, the Internal Revenue Service has delayed the filing deadline for the 2020 tax year to May 17. This is good for procrastinators, those affected by a pandemic, generational storms in Texas, or almost anyone who has private placement securities whose tax forms are notoriously late. It can also be good for wealth advisors who can be quite busy taking care of clients during filing season!

Many people get super focused on taxes at this time of the year. At TandemGrowth, we field a lot of calls from prospective clients when they get sticker shock over their tax bill. Or occasionally, one of our own clients who forgot that we did a Roth IRA conversion over a year ago when markets were low and benefits were high. It is my sad duty to report, however, that tax planning now for 2020 is about 5 months too late! Like someone buying insurance AFTER the house burned down – while the insurance is nice for the future, it won’t help replace what was already lost. The message here is tax planning should be ongoing and thought about throughout the year – but, at a minimum, before the turn of the calendar.

Having gone through the work of collecting all of the data and forms for your tax return, it can be easy to want to file the completed return away and relax knowing you will not have to do this again for a year. However, this is an excellent time to leverage the work that you and your CPA or tax software have done. Meaning, you already have a lot of data that can be useful as you plan for the current and future years.

In our firm, we are diligent in requesting filed returns from our clients. While we know our clients’ personal situations intimately, analyzing the recently filed return can reveal important planning opportunities. Or, at least, identify areas of discussion that could create real economic value.

While this is not designed to be an exhaustive list, here are

15 Potential Financial Planning Opportunities You Could Uncover from Your Form 1040:

(For reference, you can pull up a copy of a Form 1040 by clicking here.)

-

- Has something changed in your filing status and number of dependents? Are you claiming all dependents for which you are eligible?

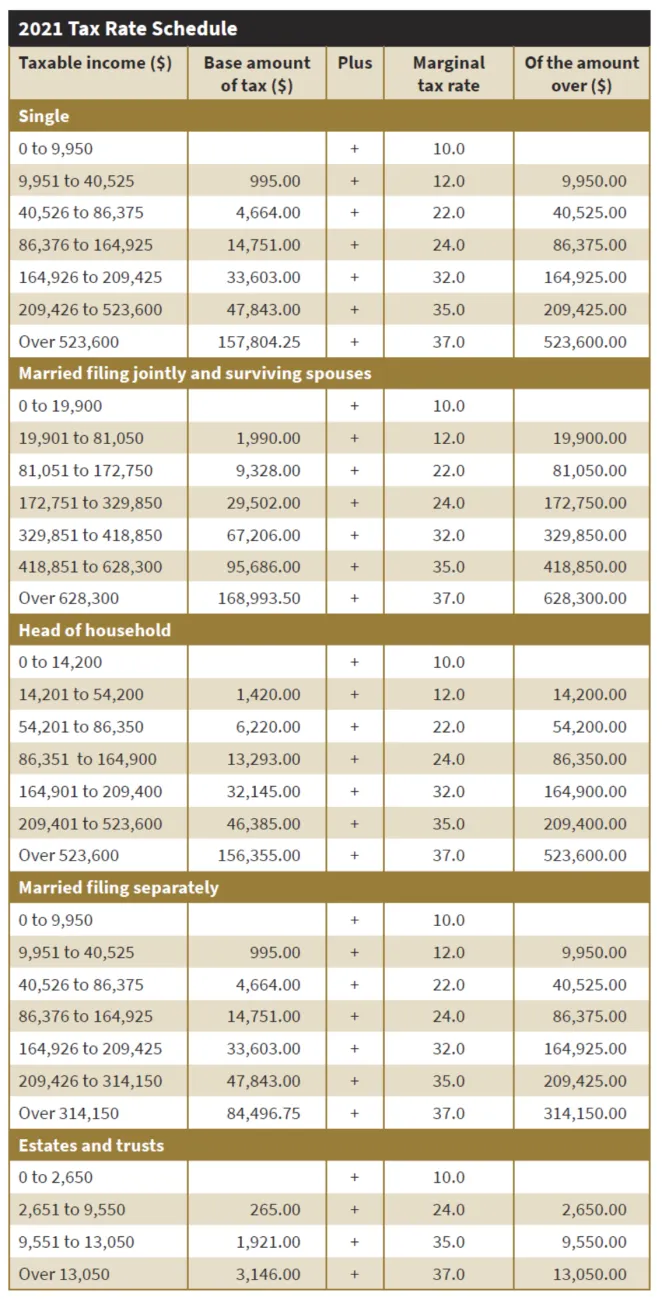

- Look at line 11b and review your taxable income. Use the table below to calculate your marginal tax bracket. This is the federal tax you pay on the last dollar that you earn. How far above the last bracket are you? Are there opportunities in the current year to lower your bracket? How far below the next bracket are you? Are there opportunities to fill up the current (potentially lower) bracket today if you expect lower than normal income in the current year or you expect higher income or tax rates in the future? (Roth conversions, etc.) You will also use the marginal rate to assess whether taxable or tax-exempt bonds should be preferred in your taxable accounts.

- In 2021, if your taxable income falls below $80,800 (Married Filing Jointly), there may be an opportunity to harvest capital gains at a 0% tax rate.

- What is your average tax rate? Divide line 16 (total tax) by line 11b (taxable income). This will give you a general idea of the percentage to have withheld from retirement plan distributions, IRAs, or how much to set aside for taxes from taxable income. You can also use this number to audit your financial planning assumptions to see if the annual tax liability assumptions in your projections are “in the ballpark”.

- Line 23. Did you owe significant taxes? If so, you may need to adjust estimated tax payments or adjust withholdings. Was the cause of the shortfall a known and “one-time event”? Were you subject to penalties for underpayment?

- Line 20. Did you get a significant refund? If so, you may want to adjust your withholdings or estimated payments. There is no reason to make an interest free loan to the government.

- Lines 2a, 2b, 3a and 3b and Schedule B show us how much you receive in interest and dividend income. We can use this information in conjunction with your marginal tax rate to assess your after-tax income from your investments in taxable accounts. It can trigger a conversation around the structure of your portfolio and whether it should be invested in more tax-exempt vs taxable bonds or more in securities that generate qualified dividends which are taxed at favorable long-term capital gains rates.

- Line 4a tells us if you took a distribution from an IRA. Line 4b will tell us if it was rolled over. If Required Minimum Distributions (RMDs) were required, it will tell us if you did a Qualified Charitable Distribution (gift). (For the 2020 tax year, the CARES Act allowed a waiver of RMDs—if you reversed yours, you, your advisor, or your CPA will want to check Form 5498 for the amount as your 1099-R will list the gross distribution even if you reversed it.)

- Schedule 3 line 8 will tell us if you make estimated tax payments. If you are required to take RMDs from your IRA (when you reach age 72 or 70 ½ if you reach 70 ½ before January 1, 2020 or with an inherited IRA) AND you make estimated tax payments, you might consider having enough withheld from your IRA distributions to cover your income tax liability and therefore no longer deal with quarterly estimates. This has several advantages over estimated tax payments: (1) the IRS treats tax withholdings as “equally paid throughout the year”, resulting in no quarterly taxes due; (2) you can make a tax withholding distribution from your IRA at the end of the year to cover your entire tax liability and avoid penalties; (3) estimated tax payment deadlines are often missed by taxpayers.

- Line 5 will indicate if you are receiving Social Security benefits, and if so, how much is taxed. Is there an opportunity to reduce income if your Modified Adjusted Gross Income is close to a bracket with lower tax on social security?

- Line 6 and Schedule D will provide clues as to how your portfolio is managed. If you realized large capital gains, was it intentional or simply due to portfolio turnover? Were these gains created to create cash flow? If used to create cash flow, when added to IRA / Pension distributions that are not rolled over, is that amount of consumption sustainable given your financial resources?

- Are there Capital Loss Carryforwards that can be used against future gains? If so, using securities sales to generate income may be more effective than owning higher yielding taxable investments or taking IRA distributions.

- Schedule 1 Line 12. Did you participate in a High Deductible Health Plan and maximize the contribution to a Health Savings Account (HSA)? An HSA is one of he most tax efficient wealth building vehicles for those that are eligible.

- Line 8b Adjusted Gross Income. If you are on Medicare, does this exceed $176,000 (Married Filing Jointly)? If so, you will pay additional Medicare Part B premiums. Are there opportunities in the current year to meet your financial goals but keep your Modified Adjusted Gross Income below these thresholds?

- Line 9. Did you itemize deductions or take the standard deduction? If you take the standard deduction, are you making charitable gifts? If so, you are not getting a charitable deduction for these gifts. Consider bunching several years’ worth of these gifts into a Donor Advised Fund and itemizing to get the tax deduction. Or, if you are over age 72 and taking required minimum distributions, consider making all charitable gifts from your IRA (Qualified Charitable Distributions) and thereby reducing your required distribution and adjusted gross income.

As you can see, a lot can be learned from reviewing your tax returns! This is just scratching the surface. A holistic wealth advisor (in partnership with your tax advisor) – one who does planning and is not just a “historian” – can help you uncover potential opportunities. Don’t waste all of your effort in preparing the return by just filing it away and not uncovering insights that could help you reduce your tax burden both now and in the future.

If you would like to learn how we integrate tax planning into your wealth management plan, our advisors stand by ready to speak with you. Simply click an image below to pull up their availability:

Jeff Bernier CFP®, ChFC, CFS

Mona Fahmy MBA, CFS, AIF®

If you’re interested in the complete copy of our 2021 Key Financial Data which includes the marginal tax bracket chart, you can find it here.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by TandemGrowth Financial Advisors, LLC), or any non-investment related content, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Moreover, you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, personalized investment advice from TandemGrowth Financial Advisors, LLC. TandemGrowth Financial Advisors, LLC is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Please remember that it remains your responsibility to advise TandemGrowth Financial Advisors, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure statement discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the terms of the engagement.