By Jeff Bernier, CFP®, ChFC, CFS

When I was a finance major at the University of Georgia, I studied the Capital Asset Pricing Model (“CAPM”). Early in my career I was trained on how to apply Modern Portfolio Theory to the construction of efficient portfolios and subsequently the Fama and French Three-Factor model which improved on the other models to further explain markets. I would spend hours using sophisticated portfolio optimization software to model various portfolio choices and build model portfolios.

At some point in the early 1990s, I saw a presentation by Nick Murray, a well-known financial adviser and author, suggesting that true financial and investment planning is a right brain, emotional process and not simply a math problem. As you may know, our industry (guilty as charged!) loves to show charts, graphs, and historical evidence. Murray counseled us to focus more on “places in the heart than places on a chart.” TandemGrowth has adopted his philosophy and we continue to believe that over a lifetime of investing, investor behavior can have more impact on the long-term success of an investment plan than the investments themselves (assuming a reasonable, diversified portfolio).

Along this same line of thinking, I was fascinated with the new study of behavioral finance. Research conducted by Daniel Kahneman, a psychologist and economist, suggested investment decisions are often driven by irrational considerations and thus managing investor behavior was more important than managing the investments themselves. He was awarded a Nobel Prize in 2002 for integrating psychological insights into economics. I believe that this philosophy has served TandemGrowth clients well over the years.

“We are prone to overestimate how much we understand about the world and to underestimate the role of chance in events.” –Daniel Kahneman, Thinking, Fast and Slow

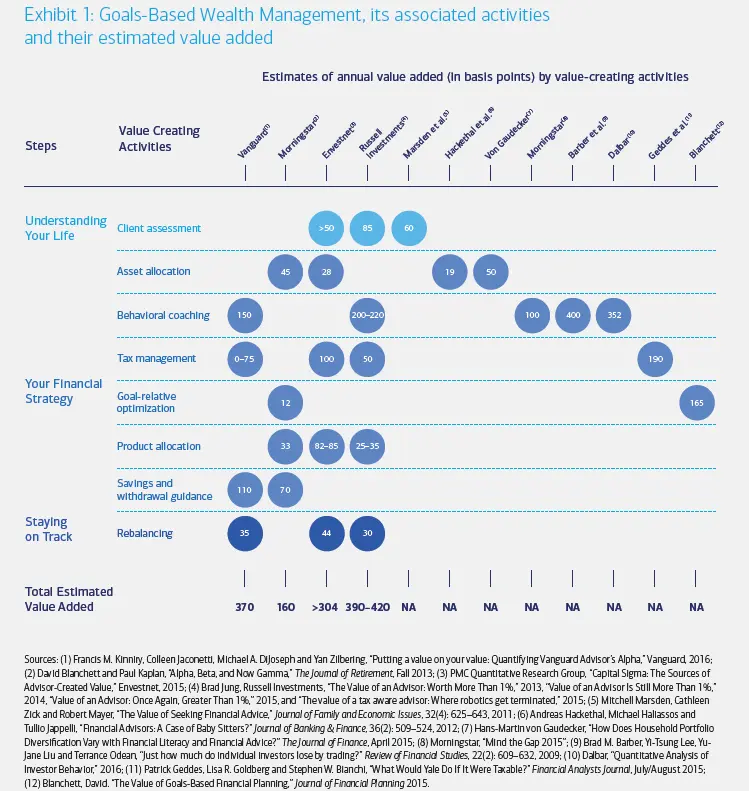

Please don’t misunderstand, the investment management craft still involves building relatively efficient long-term portfolios consistent with a client’s need, willingness, and ability to take risks. But what became obvious to me then and remains my belief to this day, is that much of the value of a good advisor is to partner with clients to encourage healthy investor behavior. (In Exhibit 1 below, Merrill Lynch gathered data from various studies and behavioral coaching consistently ranked as the highest annual value-add among value creating activities of goals-based wealth management1. On average, the studies quantifying it concluded behavioral coaching can add up to 244.4 basis points annually.)

Our industry has gone to great lengths in educating clients on the behavioral biases that can affect our investment decision making. Our firm has a short video to review some of the more important ones. My recent book The Money and Meaning Journey has a chapter on Behavioral Investing. Traditionally, however, our industry’s approach to helping you make healthier investment decisions often came from a position that you, the investor, are flawed for making the classic investment mistakes and that we, the advisor, are here to “fix you”.

Fortunately, the study and application of behavioral finance has evolved into what some are calling behavioral finance 2.0 or the “second generation” of behavioral finance. As stated in Meir Stateman, PhD’s 2019 paper Behavioral Finance, the Second Generation,

According to Second Generation behavioral finance,

- People are normal.

- People construct portfolios as described by behavioral portfolio theory, where people’s portfolio wants extend beyond high expected returns and low risk, such as wants for social responsibility and social status.

- People save and spend as described by behavioral life-cycle theory, where impediments, such as weak self-control, make it difficult to save and spend in the right way.

- Expected returns of investments are accounted for by behavioral asset pricing theory, where differences in expected returns are determined by more than just differences in risk—for example, by levels of social responsibility and social status.

- Markets are not efficient in the sense that price always equals value in them, but they are efficient in the sense that they are hard to beat.

It recognizes that people want three types of benefits—utilitarian, expressive, and emotional— from every activity, product, and service, including financial ones. Utilitarian benefits answer the question—What does something do for me and my wallet? Expressive benefits answer the question—What does something say about me to others and to myself? Emotional benefits answer the question—How does something make me feel?2

While there may be some differences in these principles and the “evidence-based” approach that TandemGrowth employs, the key insight is the need for advisory firms to be humble and empathetic to a host of client needs and wants—not just financial. (Remember, “places in the heart”.) And, an advisor can be a guide in helping clients understand the tradeoffs and costs of these benefits.

I was reminded about this evolution of behavioral finance as I was visiting with author Brian Portnoy, founder of Shaping Wealth, on The Money and Meaning Podcast in January. Brian introduced the term Funded Contentment. He defined funded contentment as the ability to underwrite a life that is meaningful to you, no matter how you choose to define that.

“Remember, successful investing is based more on minimizing regret than maximizing gains.” Brian Portnoy, CFA, The Geometry of Wealth

Shaping Wealth offers a coaching process for advisors to help their clients improve the human experience of money. A few big takeaways from Brian:

- The material abundance we seek is not a bad thing, but very incomplete in the context of seeking happy and fulfilling lives.

- Recognize that as humans, we are built to be active, to strive, to achieve. These are good things. That is the source of progress. It’s fun, it joyful. But, even when you achieve your goals, you are going to want that next thing.

- Can we, the advisory community, stop pathologizing natural human behavior and calling it “irrational”?

- Simplifying the complex. Our brains were not wired for dealing with all of this.

- The calling of the modern financial advisor is not just as mechanic but also to serve as the guide. It is one thing to build the vehicle, and to make sure the engine is running (the investments, the tax plan, the estate plan), it’s another thing to ask if the vehicle is pointing in the right direction.

- While goals are about the future, funded contentment is about enjoying the journey – the Now.

At TandemGrowth, we are using these principles to improve the client experience with the goal of helping our clients have the clarity and confidence to lead a great life. Recently I was honored to be a guest on Dr. Daniel Crosby’s Standard Deviations podcast to discuss some of these ideas and my book, The Money and Meaning Journey. Check out the Standard Deviations Podcast here.

“Humans are wired to act; markets tend to reward inaction.” –Daniel Crosby, Ph.D., The Behavioral Investor

Are you ready to partner with a financial coach to design your financial plan and invest rationally and not emotionally? Click here to get started!

1 https://behaviorquant.com/wp-content/uploads/2021/05/Merril-Lynch-2016-The-Value-of-Personal-Fiancial-Advice.pdf

2 https://www.cfainstitute.org/en/research/foundation/2019/behavioral-finance-the-second-generation