By: Jeff Bernier, CFP®, ChFC, CFS

The most important thing about an investment philosophy is that you have one you can stick with. David G. Booth[i]

If you don’t know who you are, Wall Street) is an expensive place to find out. Adam Smith (George J. W. Goodman)[ii]

Jeff, What Are You Doing with Your Portfolios in This Environment?

This is a question I get asked occasionally. It could arise at any point in time since the term “this environment” encompasses various timeframes, each presenting a distinct set of circumstances. Of course, today, the questioner could be referring to any number of real and imagined concerns as “this environment”: persistent inflation, rising interest rates, home prices coming back to earth, political wrangling over spending and debt, economic activity slowing, or a “narrow market”, among others.

My responses may not fully satisfy the questioner. Why? It’s because fruitful investing does not revolve around merely reacting to market fluctuations or the prevailing environment. Instead, it entails implementing a disciplined investment approach that seizes the growth opportunities presented by the global economy, which benefit those who hold high-quality assets. It involves a strategy that enables the compounding of earnings, dividends, and values of great businesses to compound. As wisely expressed by Charlie Munger[iii], not interrupt it (the compounding) unnecessarily.

To stick to a plan, it is crucial to have confidence in the fundamental principles of the strategy. This is especially important considering the constant pressure from financial media, well-meaning friends, or even our own anxieties, urging us to take action—any action! Furthermore, advisors often feel compelled to “Do Stuff” to justify their fees. I recall attending an industry conference where an advisor shared that she rebalanced her clients’ portfolios on a quarterly basis, solely to create the illusion of activity and make her clients believe that she was providing valuable services. Rebalance quarterly if the evidence supports that this adds return or manages risks, but doing anything solely for appearances is undoubtedly not in the best interest of the client.

During our Collaborative Portfolio Design meeting, I thoroughly delve into TandemGrowth’s investment philosophy with new clients, leaving no stone unturned (some may even find it painstakingly detailed). As a firm, we consistently reaffirm our commitment to these principles. While “doing nothing” is often the correct approach, there may be instances where new and compelling evidence arises, prompting us to improve the implementation of our philosophy through incremental refinements. Nevertheless, the threshold for making changes should be set quite high.

Recently, I have found myself even more focused on the underlying principles for two specific reasons. Firstly, as mentioned earlier, the performance of the U.S. equity market this year has been primarily driven by a select few companies. Secondly, Dimensional Fund Advisors has recently published their latest editions of the Matrix Book and The Fund Landscape 2023.

“Revenge of the Turds”

Similar to the bursting of the tech bubble in 2000, this year we are witnessing a scenario where broadly diversified portfolios lacking significant exposure to a handful of tech stocks are experiencing underperformance. While the average stock has remained relatively flat throughout the year, the top seven stocks have surged by 53%. It raises the question: Could the current mania surrounding Artificial Intelligence potentially resemble the dot-com bubble of the late ’90s?

In an article humorously titled “Revenge of the Turds,” Chris Satterthwaite, CFA highlights the remarkable rise of low-profitability, high-investment stocks: “Low profitability, high investment stocks are on a tear. Garbage stocks are back!” The emergence of technologies like ChatGPT and the widespread enthusiasm for artificial intelligence have fueled a substantial rally in unprofitable tech companies.

However, it is essential to recognize that historically, such trends have not ended favorably for investors who disregard the enduring principles of “what always works” given sufficient time. Instead, succumbing to the fear of missing out (FOMO) and abandoning a diversified approach based on recent underperformance can prove detrimental.

As I discussed in my book, The Money and Meaning Journey, it is evident that in the short term, investor sentiment and the collective actions of the herd can overpower fundamental factors. However, as aptly stated by Benjamin Graham, “In the short run, the market is a voting machine; in the long run, a weighing machine.” Ultimately, the market evaluates and measures the true worth of investments based on their underlying fundamentals.

When a new client presents me with an investment statement containing various individual stocks and bonds, accompanied by the claim that these were recommended by their previous advisor, I immediately recognize a stark contrast in philosophy between that advisor and our own approach. In the past, these statements would often display brokerage firms’ analyst “ratings” for these stocks, sometimes indicated by letter grades like A or B+. This may have provided a sense of reassurance to clients, suggesting that these stocks were meticulously researched and deemed as sound investments by the investment firms’ analysts.

However, in the early 2000s, much of this practice was discredited when it was revealed that these firms frequently recommended stocks of their investment banking clients. A notable example is Enron, a Wall Street “Darling” that was crowned “America’s Most Innovative Companies” by Fortune Magazine for six consecutive years, from 1996 to 2001. Sadly, shortly thereafter, Enron experienced a dramatic downfall, culminating in its ultimate failure and bankruptcy.

There is a continuum that runs from active stock picking with a handful of stocks on one end and a Total Market Index Fund on the other. I think it is important for investors to know where an advisory firm sits on this continuum.

The Mutual Fund Landscape 2023

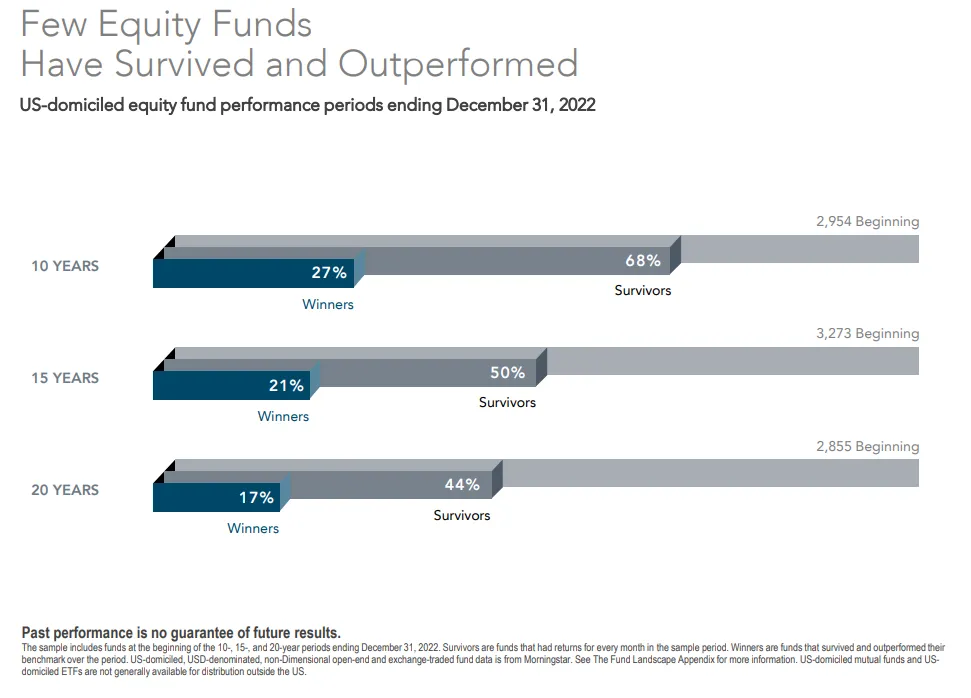

On the continuum, positioned to the right of the limited “stock pickers” portfolio, we have advisors who opt for actively managed pooled accounts such as mutual funds, Separately Managed Accounts (SMAs), or sub-accounts within annuities. The underlying belief is that, through careful selection and timing, one can achieve superior performance by utilizing traditional active management strategies. However, this assertion is challenged by research conducted by The Standard and Poor’s SPIVA[iv] and The Dimensional Fund Advisors Mutual Fund Landscape report. According to the 2023 Mutual Fund Landscape report, only 17% of actively managed mutual funds and ETFs managed to survive and outperform their respective benchmarks over a 20-year period. It is important to note that it is impossible to predict in advance which specific 17% will achieve this feat. For a concise overview of these findings, you can watch a short video available here.

If you recognize that traditional active management may not consistently add value to your portfolio over time, you might choose to collaborate with an advisor situated at the far-right end of the continuum. Such an advisor is likely to construct your portfolio using passive index funds, and they may even prefer a more streamlined approach by investing in broadly diversified total market funds. From our perspective, this approach represents a significant improvement compared to the philosophies of active stock picking or actively managed funds.

Index funds possess desirable characteristics that align with our strategy: low costs, tax efficiency, and diversification. However, we believe there is room for improvement. Although index funds are labeled as “passive,” they still track a list of securities created by someone else—the index provider, such as Standard and Poor’s or Russell. Moreover, since these products generally allocate holdings based on market capitalization, there is a possibility of ending up with a portfolio heavily weighted towards a few sectors and overweighting the most expensive and popular stocks.

Exploring the Matrix Book and our Investment Philosophy

At TandemGrowth, our investment philosophy veers slightly left of the total market index position on our hypothetical continuum. This approach can be described as systematic active or factor tilted. Leveraging research findings from our trusted investment partners, we construct diversified portfolios with low costs and tax efficiency, strategically “tilting” towards securities that peer-reviewed, academic research indicates have higher expected returns. The Dimensional Fund Advisors Matrix Book serves as a valuable tool for assessing these differences.

As part of our strategy, we incorporate Dimensional Fund Advisors products into our portfolios. These products systematically adjust the underlying holdings, favoring securities that have historically delivered higher returns, such as value stocks, small companies, and more profitable companies. To gauge the performance of these strategies over time, Dimensional Fund Advisors constructs indexes that replicate this formula.

The Matrix Book serves as Dimensional’s annual survey of investment performance. Drawing on historical data, it transcends short-term market fluctuations and provides insights into the dimensions that explain variations in returns. (Click here to download a copy of the Dimensional Fund Advisors 2023 Matrix Book)

Let’s examine the growth potential of a $1 investment over the long term:

- A $1 investment in The Standard and Poor’s 500 Index in 1926 would have grown to $11,527 by the end of 2022.

- A $1 investment in the Dimensional US Adjusted Market 2 Index, which incorporates factor tilting, in 1928 would have grown to $18,159 by the end of 2022.

- A $1 investment in the Dimensional US Small Cap Index in 1928 would have grown to $41,204 by the end of 2022.

- A $1 investment in the Dimensional Small Cap Value Index would have grown to $128,147 by the end of 2022.

It is important to note that these examples, sourced from Dimensional Fund Advisors’ 2023 Matrix Book (pages 42-45), do not imply the existence of a magical formula for higher expected returns. Instead, the higher expected returns are for bearing additional, compensated risks. Some factors may exhibit higher expected returns due to investor behavioral errors. The key takeaway is that there are more reliable ways to improve expected returns than relying on guesswork when selecting a handful of stocks or which active manager might “outperform.”

Why This Matters

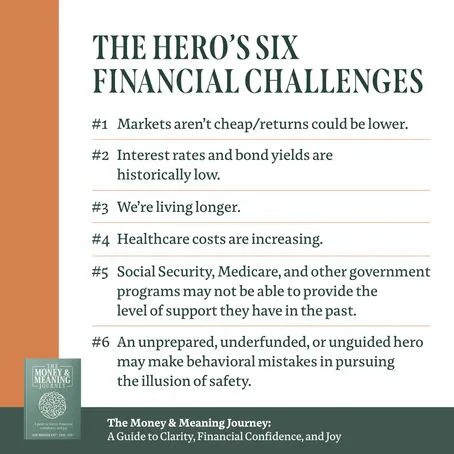

In The Money and Meaning Journey, I explored the six financial challenges faced by my “Hero” as they navigate Act 2 of their lives. It underscores the importance of addressing these challenges to foster a confident and secure future. The recipe for success includes effectively managing emotions, defining priorities based on what truly matters, diligent planning to safeguard and grow wealth, and striking a balance between spending less and the potential for higher volatility or expected returns. Increasing exposure to factors beyond a passive “index” strategy can potentially be beneficial in achieving these goals.

Mathieu Pellerin, PhD, Senior Researcher and Vice President at Dimensional Fund Advisors, recently emphasized this point in a paper that highlights the benefits of targeting factors such as size, value, and profitability to improve retirement outcomes. For a summary of the article, you can refer to this link, and for the full 12-page paper, click here. You can also listen to a podcast in which Mathieu discusses these points.

As goal-focused and planning-driven investors, we adhere to three key principles that 50-year industry veteran Nick Murray, the financial advisers’ adviser, identified as fundamental for long-term investment success:

Faith in the future and the capital markets. The evidence supports this belief. I’ve never known a successful investor who lacked this quality.

Patience. This is a most un-American quality. The key, as Kipling said, is the ability “to keep your head when all about you are losing theirs”[v] and to give a sound strategy time to work.

Discipline. You must apply the strategy and behaviors consistently over time.

Please reach out if you have questions, comments or would like to learn more about Tandem Growth Financial Advisors Investment or planning philosophy.