By: Jeff Bernier

“Winter Is Coming”

If you visited the Dairy Queen restaurant in Fargo, North Dakota to see the world’s largest Dilly Bar in July, you would be welcomed by average temperatures between 60 and 80 degrees Fahrenheit. If you asked the employee behind the counter if the weather is always like this, he or she might say, of course, in July! If the experience was so life changing that you told them you’d like to come back every 6 months to commemorate this seminal moment in your life and asked them what to wear in January, they would probably not suggest shorts and a t-shirt. You (nor they) would be surprised to know that the average temperature in Fargo in January is from -1 to 16 degrees Fahrenheit. And it happens every year.

Do you think the people of Fargo get upset about this every year? I doubt it. The arrival of winter surprises no one.

The motto of House Stark in the television series A Game of Thrones was “winter is coming” and refers to their vigilance. It is an expression that means one should always be prepared. As rulers of the North, they must always be ready for anything that could happen – and eventually something will. Thus, winter is coming.

Of course, Winter is always coming, and we are not surprised or overly concerned by its arrival. It is normal.

I thought about this as I watched a presentation by Dr. Lacy H. Hunt of Hoisington Investment Management at the National Association of Personal Financial Advisor National Conference in May. Dr. Hunt is a respected economist and commentator on the economy and Federal reserve policy. In addition to a lengthy career with major financial institutions, he served as a senior economist at the Federal Reserve Bank of Dallas. A Texan with gray in his hair, this is not his first “rodeo.” He is a “straight shooter” – he calls it like he sees it.

The big question that he pondered: Will the Federal Reserve do what is necessary to mitigate the current inflation problem, even if it puts us into a recession (shallow, normal, or deep) in the face of political pressure?

Sen. Warren warns Fed Chair Powell not to ‘drive this economy off a cliff’[i]

Dr. Hunt began his talk with insights and reminders of how we got here[ii]:

- The Federal Reserve came to the rescue during the Great Recession (2007-2009) with non-traditional monetary policy to save the patient. (The U.S. and the global economies were in the intensive care unit.)

- Since the year 2000, the U.S. economy has grown at a rate of approximately 50% of its normal rate going back to the late 1800s.

- The negative effects of the U.S. debt levels are influencing GDP.

- Low rates and low inflation emboldened governments to run deficits.

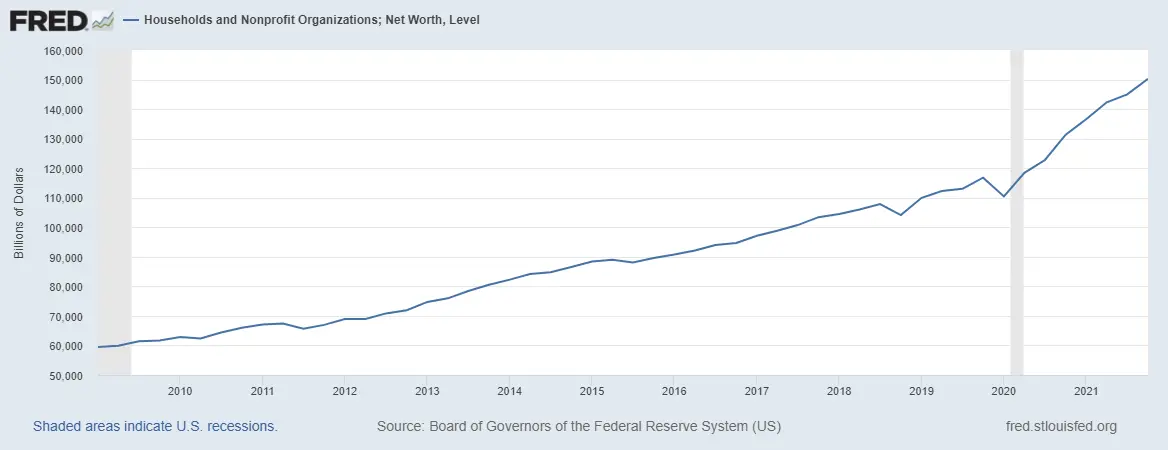

- Due to accommodative monetary policy (artificially low interest rates) and the Fed “put” (the Fed comes to the rescue whenever markets misbehave), financial assets and residential real estate have experienced significant growth. (Since 2011, household net worth grew from $60 billion to $150 billion as you can see in the chart below.)

- Therefore, if you are an investor or homeowner, it is likely that your portfolio or home value is larger than it would have been without these accommodative polices.

- These benefits did not grow evenly across all citizens. The wealth divide has gotten larger.

- Due to the Covid-19 shutdown and deep (short) recession, the Fed and Congress came with massive additional stimulus and liquidity.

- After the economy appeared to be out of the woods, the Fed continued bond purchases and kept rates low while Congress continued to pass more spending.

- The result of these policies (Dr. Hunt believes policy errors) in addition to other factors (supply chain, geopolitical risks, etc.), we are now experiencing massive inflation that must be dealt with.

- We are now paying the “bill” in terms of higher inflation and the Federal Reserve “taking the punch bowl” away.

We often refer to the Federal Reserve’s “dual mandate.” Dr. Hunt reminded us that the Fed really has three goals. Under the Federal Reserve Reform Act of 1977, the Fed expanded its role to “the goals of maximum employment, stable prices, and moderate long-term interest rates.” The real tradeoff today is between stable prices and employment. He believes that more people are affected by persistent inflation than the jobs that were created by the policies of late:

“The imbalance between those who benefitted and those who were harmed from the monetary and fiscal policies pursued over the last two years is abundantly clear. The 8.5% inflation rate has dramatically lowered the standard of living of over 170 million individuals. When this circumstance is compared with the accomplishment of the objective by monetary and fiscal authorities to lower the unemployment rate from a recession high of 14.7% in April of 2020 to 3.6% today, the fallacy of twin mandates is abundantly clear. The lowering of the unemployment rate reflected the creation of 20.4 million new jobs. Is it a fair balance to help 20 million individuals at the expense of permanently harming 180 million?”[iii]

While Dr. Hunt indicated that the actions of the Fed were appropriate and necessary during the early stages of the pandemic, he faults the Fed with not recognizing the longer-term inflation. If you will recall, for several months the Federal reserve and some politicians continued to use the term “transitory.”

Another view was published by Kenneth Rogoff in May in The Project Syndicate. He argued that the Federal reserve had little choice due to political pressures. Jerome Powell was reappointed in November. It is possible that any change in policy that might hurt the economy in the short run would have been damaging to his reappointment. From the article: “Moreover, progressives were enthralled by the idea that US federal debt could rise substantially without triggering a significant increase in inflation or interest rates.”

Dr. Hunt made two other memorable points:

- When inflation is tolerated, it undermines growth and leads governments further in the direction of “central planning / command and control” which reinforces the upward growth in government and the private sector shrinks.

- Monetary controls (tightening cycles) have resulted in recessions 90% of the cases since 1913. (The Fed’s founding)

“Winter”, I mean, Recessions are Normal

Like the fine people of Fargo are about winter, we should also be a bit “stoic” about recessions. While they are not enjoyable – they are normal. The United States has experienced eight recessions in the last 50 years. Therefore, you should statistically expect one about every six years.

A recession is not something to be feared – it is something to be prepared for. (Winter is coming.) Here is a piece of important historical data: In 1970, the S&P 500 Index of large U.S. corporations was trading at 90. Today, it is trading around 4,000. Despite eight economic downturns, an investment in the great businesses of the U.S. compounded at 7.5 percent per year – not including dividends paid out to the owners (10.64% including dividends). The income paid out to shareholders grew at 6% per year – outpacing inflation.[iv]

Prices adjust quickly to reflect current information. Possibly due to investor psychology, sometimes aggregate prices fall further than earnings. In the long run, the value of businesses follows the growth in earnings and the growth in earnings is the result of economic growth. In the short run, markets are highly influenced by sentiment. (Benjamin Graham’s voting machine). In the long run, it is influenced by earnings (Benjamin Graham’s weighing machine)[v]. Equity markets are also considered “leading” indicators – declining before an economic recession is declared and recovering before the “all clear” sign or the economic recovery shows up in the statistics.

Therefore, the long-term investor is encouraged to think like an “opportunist” and not a “victim.” What I mean by this is recessions are historically the best time to invest as prices reflect the current reality and therefore: falling prices = greater value = higher expected returns. This creates an opportunity to compound future earnings at lower prices.

Now don’t get me wrong – market downturns and recessions are not enjoyable and certainly can be scary. They can be tragic and stressful for someone who loses a job and is not prepared. But, for the long-term investor who does not “have to sell”, accepting “what is” and understanding how normal this all is (the stoic mindset), can be helpful.

The Bear Market

As the Fed attempts to take the “punchbowl” away by raising the Fed Funds rate, reduce asset purchases (QE), and recession fears grow, asset prices react. We are now in a “bear” market. Traditionally defined as a 20% or greater decline in equity markets. Even more concerning for the “balanced” investor, quality bonds are down over 11%.[vi]

It is an interesting and confusing time. If you are feeling a little uneasy, it is understandable. Someone asked me recently, “When will the stock market get back to normal?” It was my sad duty to report that a 20% decline every few years IS normal. “Bear Markets” are not a “flaw”, they are a “feature.” They are the necessary price to pay for the growth mentioned before—7.5% compounded growth, 6% growth in dividend income. What seems a bit “abnormal” to me is a 70% advance in the S&P 500 during a global pandemic!

S&P 500 Calendar Year Results

2019 28.88%

2020 16.26%

2021 26.89%

While equity markets are in “bear territory”, if you are not diversified and concentrated your portfolio in a handful of the most popular “stay at home” stocks, crypto currencies, or long duration assets (long-dated zero-coupon bonds), this may feel like a depression. According to Ben Carlson at A Wealth of Common Sense, in May almost 10% of the Russell 3000 Index was down 90% from their highs and nearly 1 in 5 were down 80% from their all-time highs![vii]

The Case (gulp) for Bonds (A Diversified Portfolio)

I love being a shareholder in the world’s great businesses. Historically, you accrete real (after-inflation) wealth. You share in global growth and profits. If preservation of purchasing power is the objective (and how could it not be for the clear-thinking retirement investor?), stocks provide better defense than bonds. However, to be an all-equity investor, you must be psychologically prepared for a 50% downturn periodically. It is my view that most investors cannot stomach this level of volatility and are likely to make significant behavioral mistakes (liquidate near the bottom) for which their financial plan would never recover. Therefore, bonds have historically provided some “defense.” Despite the messy transition we are in, the real possibility of a recession and the higher yields (and expected returns) of fixed income investments, make a diversified portfolio with high quality fixed income investments likely advisable to the long-term investor.

This Too Shall Pass

The great investor John Templeton is widely quoted as stating that the four most dangerous words in investing are “This time it’s different.” Financial commentator Nick Murray frequently states that a corollary to this and the four most useful words in investing are “This too shall pass.”

You may find some of this interesting but now ask – what do we do with all of this? Here are a few reminders of things that are always “in season” but even more so during “winter”:

- Have a holistic financial plan that assumes realistic long-term returns and expects periodic bear markets

- Think like an opportunist and not a victim

- Remember that price and value are inversely related – expected returns have improved

- Re-balance portfolios

- Tax loss harvest where appropriate

- If considering a Roth IRA conversion, consider completing when prices have declined

- If employed, maintain adequate cash for emergencies and potential job losses in a recession (have a “Plan B”)

- If retired, maintain a short-term portfolio to help address “sequence of return” risks

- Keep investing – compound earnings power at more compelling prices

- Maintain margin: having room in your budget for the unexpected (I love Morgan Housel’s recommendation – “save like a pessimist, invest like an optimist”)

- Focus on things you have control over that matter and not on things you have no control over or that don’t matter

- Be grateful and generous with your time, talent, and treasure. (Don’t expect a financial reward but the energy and perspective this provides is priceless)

- Be judicious with your time on financial media / journalism.

- Go live your life and enjoy the journey. The past is for learning, the future can motivate us, but we live in the NOW!

If you’d like to discuss any of this in further detail or if you’re ready to develop a customized financial map of your own, please do not hesitate to reach out to us:

|

|

|

|

|

[i] https://www.marketwatch.com/story/sen-warren-warns-fed-chair-powell-not-to-drive-this-economy-off-a-cliff-2022-06-22?mod=bnbh Published: June 22, 2022 at 10:21 a.m. ET

[ii] I have added a few items to this list to fully expand the idea.

[iii] Hoisington Investment Management, Quarterly Review and Outlook First Quarter 2022

[iv] http://www.econ.yale.edu/~shiller/data.htm

[v] The father of value investing, Benjamin Graham, explained that in the short run the market is like a voting machine – adding up which companies are popular and unpopular. But in the long run, the market is like a weighing machine – assessing the substance of a company.

[vi] iShares Core U.S. Aggregate Bond ETF

[vii] https://awealthofcommonsense.com/2022/05/15-of-the-craziest-charts-right-now/